In an increasingly unpredictable market landscape, quant funds are uniquely positioned to manage and capitalize on volatility. Their strength lies in the combination of systematic models, adaptive risk controls, advanced analytics, and thoughtful human oversight. Together, these elements help build portfolios that remain resilient across cycles while aiming to deliver risk-adjusted performance.

SYSTEMATIC AGILITY & REGIME ADAPTATION

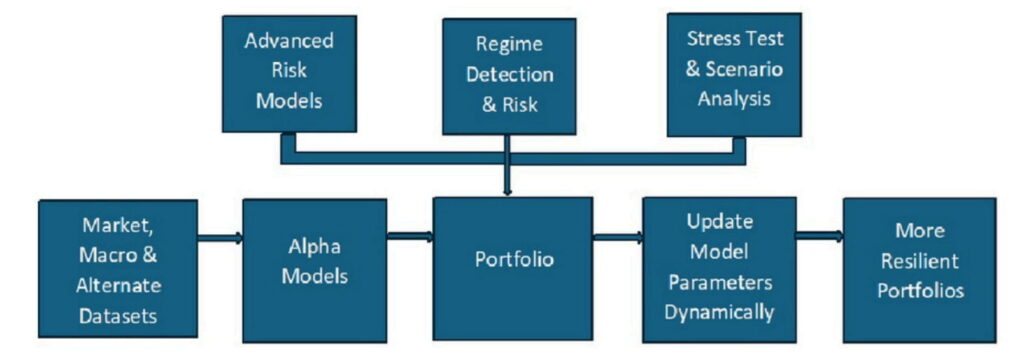

Quant funds use pre-defined, rigorously tested models whose parameters are updated with respect to changing market conditions, ensuring portfolios stay aligned with shifts in price, volatility, and liquidity. These models continuously monitor and estimate different market regime probabilities, whether trending, sideways, or stressed and adjust exposures accordingly. Predictive analytics estimate the likelihood of tail events and automatically activate crisis-mode controls, scaling back positions and strengthening capital protection.

SHARPER DIVERSIFICATION. STRONGER RISK DEFENSE

Beyond traditional diversification, a multi-factor approach enables quant strategies to spread risk across a broader set of non-traditional and macrodriven factors. Risk models continually measure exposure to style, sector, and macro risks, ensuring the portfolio remains balanced and not overly dependent on any single driver of returns. Advanced statistical techniques monitor subtle changes in correlations and factor behaviour, identifying hidden risk clusters that traditional analysis may miss. To strengthen early detection further, quant strategies incorporate alternative data — sentiment, liquidity patterns, and structural signals — providing additional foresight into rising vulnerabilities.

FORWARD-LOOKING RISK MANAGEMENT WITH HUMAN OVERSIGHT

Quant funds run continuous scenario analysis and stress simulations to assess how portfolios may respond to shocks such as GFC, Covid Crisis, etc. This proactive, simulation-driven approach enables risk adjustments before problems materialize. Importantly, all automated insights are reviewed by experienced investment and risk professionals, who validate model behaviour, enforce liquidity and position limits, and ensure judgment and governance guide the systematic process.

THE QUANT ADVANTAGE

Quant funds don’t avoid volatility — they manage and harness it. By combining adaptive models, diverse return sources, and proactive human-guided risk control, they aim to deliver more resilient portfolios, fewer deep drawdowns, and long-term risk-adjusted

performance across market cycles.

Disclaimer: Views expressed herein involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied herein. This communication is for informational purposes only and should not be construed as investment advice or a recommendation to invest in any scheme or product. There is no assurance of any returns/capital protection/capital guarantee to the investors in the abovementioned funds. AlphaGrep Investment Management Private Limited shall have no responsibility/liability whatsoever for the accuracy or any use or reliance thereof on such information.

Investors are requested to read all scheme-related documents carefully before investing. Investments in Mutual Funds or any financial products are subject to market risks.